February 2024 was a positive month for the new car market in Europe. According to JATO Dynamics’ data from 28 European markets, a total of 988,116 passenger cars were registered during the month. This marks a 10% rise in volume compared with February 2023, bringing the year-to-date total to nearly two million units – an increase of 11 percent.

According to Felipe Munoz, Global Analyst at JATO Dynamics: “As the economic outlook has continued to improve, the car market has gone from strength to strength. This comes despite the ongoing geopolitical tensions across the continent.”

However, Battery Electric Vehicles (BEVs) are not driving growth as they historically have done. In contrast, petrol cars performed almost as well as they did before the Covid-19 pandemic. JATO’s data revealed that these vehicles were responsible for 61% of total sales in February 2024, in comparison to the 62% registered in February 2019. This success comes at the expense of diesel cars, with the market share of these vehicles falling from 35% of registrations in February 2019 to just 15% last month.

Munoz added: “Despite the noticeable shift towards EVs, many European consumers are not ready to turn away from ICE cars. While we’re seeing a clear decline in demand for diesel models, drivers are opting for gasoline alternatives, rather than switching to electric.”

Chinese-made cars drive growth

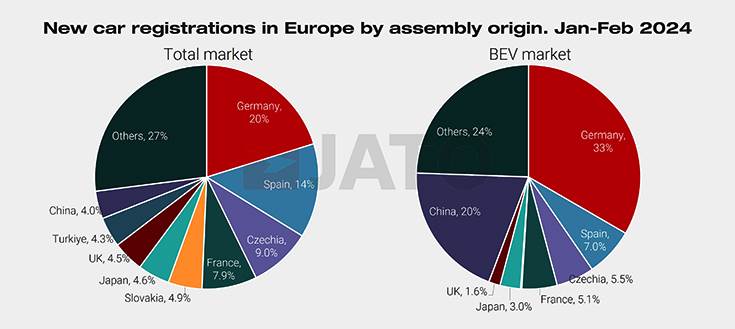

In Europe, sale of cars made in China saw the highest levels of year-on-year growth in February 2024 (+45%) and in January-February 2024 (+43%). By comparison, the registrations of cars made in Germany and Spain – the second and third most popular origins – saw increases of 6% each during February.

This is the highest increase among the top 10 origins – allowing the market share for these vehicles to reach 4.0%, up from 3.0% in February last year. As a result, cars made in China outsold cars made in Italy, Korea, Morocco, and Romania, while also closing the gap between cars made in Turkey and the UK.

This growth is even stronger when looking at BEV registrations, with cars made in China accounting for one in five BEV registrations in February and January-February. In contrast, registrations of BEVs made in Germany increased by just 8% in the first two months of this year. The volume of plug-in hybrid cars made in China fell by 62% last month, with these vehicles making up just 3.4% of the total coming from China, compared to 66% for BEVs.

Commenting on the same, Munoz said: “The growth is partly explained by action taken by some Chinese OEMs to accelerate imports ahead of the EU decision on the anti-subsidy investigation. Increased tariffs could slow the growth of China’s OEMs, but as a knockon effect it could also prompt them to accelerate their deliveries to Europe.”

While these results are impressive, it is notable that approximately 44% of all the volumes of made-in-China cars were registered by Western brands including Tesla, Volvo, and Dacia, while 40% were registered by MG – fully Chinese-owned and designed, but positioned as a UK brand in the West. This means that Chinese brands accounted for just 16% of Chinese-made cars registrations, reinforcing the fact that these manufacturers continue to face challenges related to perception and awareness in Europe.

Munoz added: “Chinese brands still have a long way to go before they occupy a significant part of the European market. Despite the strides they have made in regard to performance and affordability, increasing awareness and shifting longstanding perceptions will take time.”

MG gains traction

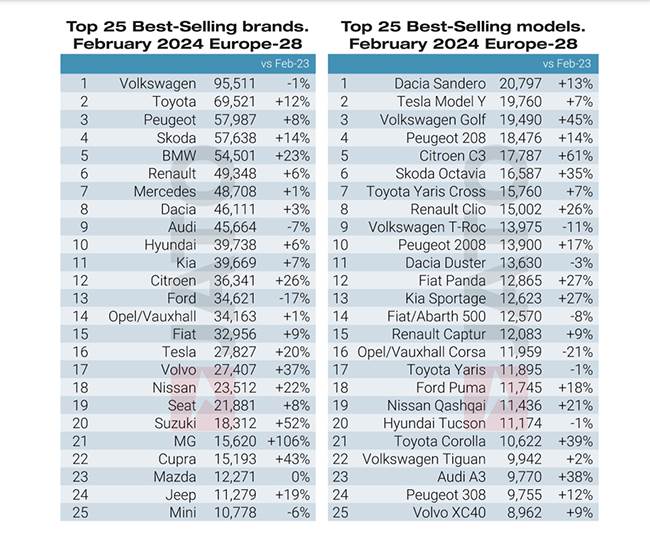

SAIC, the parent company of MG and Maxus, continued to climb the rankings in February. Due to the popularity of its combustion engine models, it secured the highest market share increase of any OEM in February. Despite the strong performance of its electric models (the MG 4 was the fourth most-registered electric car in February), petrol models were the main driver of growth for the manufacturer. As a result, MG registered more new cars than Cupra, Mazda, or Jeep during the month.

Other big players in February included Suzuki, BMW Group, Mitsubishi, and Toyota. In contrast, Volkswagen Group, Ford, Renault Group, Mercedes, and Hyundai-Kia posted the biggest losses in market share.

Dacia’s Sandero leads the charge

The Dacia Sandero retained its position as the most registered car in Europe for the second month in a row, with 20,800 units registered – an increase of 13% compared to February 2023.

The Tesla Model Y fell behind, having been the most registered passenger car in Europe last year while strong demand in key markets saw the Volkswagen Golf take third place.

Registrations of Citroen’s C3 increased by 61% from February 2023, in part due to the competitive deals offered on the previous generation and prices introduced by the OEM as the new generation arrived. The Skoda Octavia, Toyota Corolla, Audi A3, BMW X1, Seat/Cupra Leon, Tesla Model 3, MG Zs, and Opel/Vauxhall Astra also saw a rise in registrations.

Among the latest entries, Jeep registered 5,677 units of the Avenger, 1,434 of which were electric. Volvo registered 3,663 units of the EX30, and Renault registered 1,722 units of the Espace. Mitsubishi registered 1,535 and 1,339 units of the Colt and the ASX, respectively, and Honda registered 1,100 units of the ZR-V.